This week, the domestic aluminum scrap market showed an upward fluctuation pattern, with the price center slightly rising in line with primary aluminum movements. By October 23, the SMM A00 aluminum price closed at 21,040 yuan/mt, up 90 yuan/mt WoW. As the traditional peak season draws to a close, tight aluminum scrap supply remains the main theme, with procurement challenges for aluminum tense scrap in Hubei becoming prominent. Prices for shredded aluminum tense scrap and machinery aluminum tense scrap increased by 100 yuan/mt in a single day, followed by two consecutive days of increases. On the other hand, a recycling enterprise in Henan lowered prices for aluminum scrap used in profiles by 300–500 yuan/mt, reflecting diverging downstream demand and weakness in certain sectors. The price difference between primary metal and scrap continued to widen, with the spread for machinery aluminum tense scrap in Shanghai expanding from 2,212 yuan/mt at the start of the week to 2,302 yuan/mt, while the spread for aluminum used in profiles in Foshan also widened to 2,299 yuan/mt. On the macro front, tax filing for secondary aluminum enterprises was delayed until the end of October, uncertainty over the cancellation of tax rebates increased, and market sentiment turned cautious amid disruptions from Trump's tariff threats. Next week, the aluminum scrap market is expected to hold up well, with the mainstream price range for shredded aluminum tense scrap (water price) hovering around 17,500–18,000 yuan/mt. If the primary aluminum price stabilizes above the 21,000 yuan/mt mark, it will further transmit positive effects and support aluminum scrap prices, while the tight supply situation is unlikely to change in the short term. Demand side, resilience remains in sectors such as NEV and PV, but the end of the traditional peak season and high social inventory pressure may curb procurement enthusiasm. Close attention should be paid to the restocking pace of secondary aluminum enterprises after the holiday and the sustainability of end-use demand. If the primary aluminum price retreats after a rapid rise or downstream demand weakens too quickly, the aluminum scrap market may face pullback pressure. Overall, the market will continue its tug-of-war between sellers and buyers, requiring close monitoring of primary aluminum trends and policy developments.

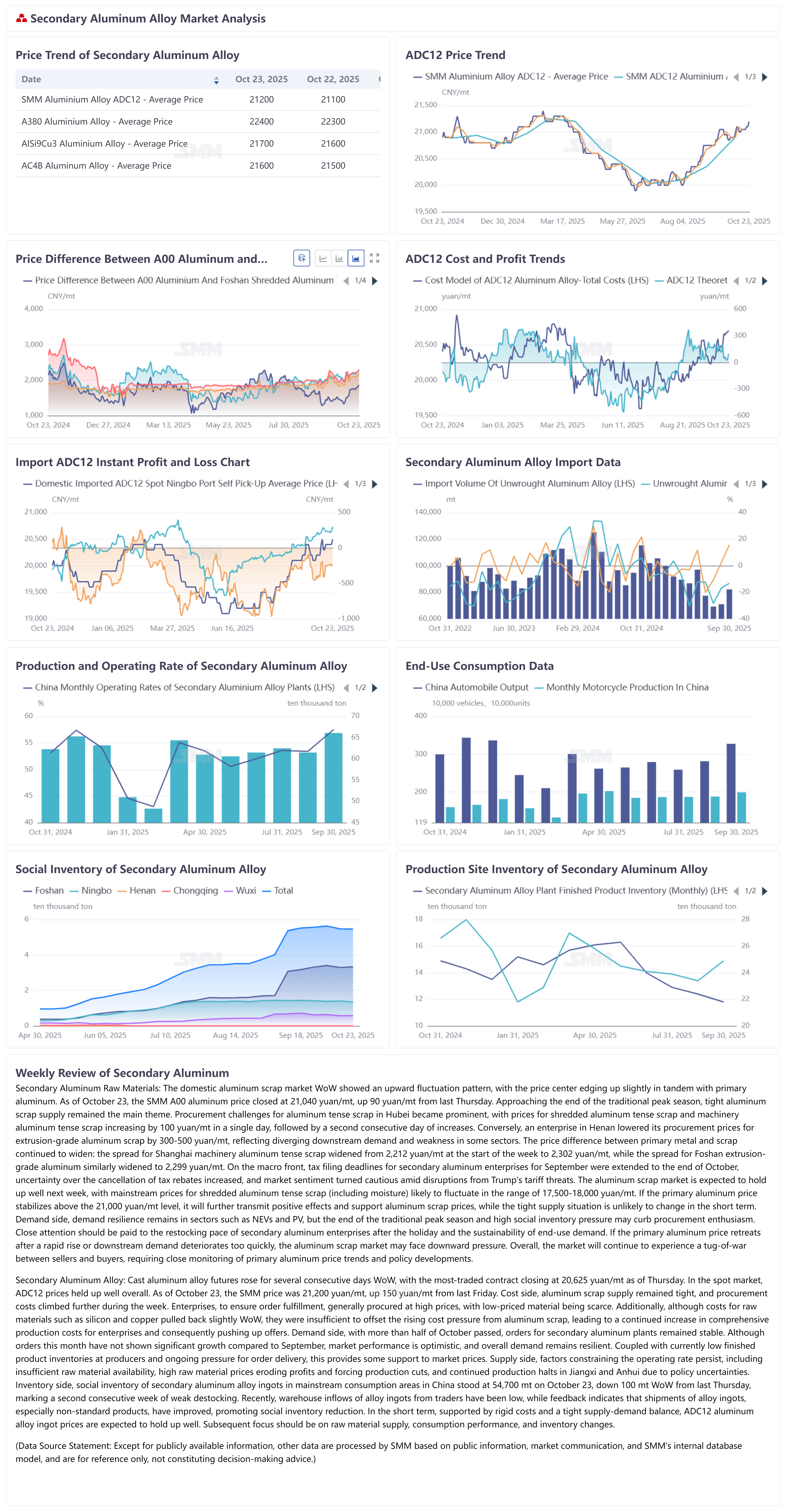

This week, cast aluminum alloy futures rose for several consecutive days, with the most-traded contract closing at 20,625 yuan/mt as of Thursday. In the spot market, ADC12 prices held up well overall, with the SMM offer reaching 21,200 yuan/mt as of October 23, up 150 yuan/mt WoW. Cost side, aluminum scrap supply remained tight, and procurement costs climbed further during the week. To ensure order fulfillment, enterprises generally purchased at high prices, while low-priced sources were scarce. Additionally, although the costs of raw materials such as silicon and copper pulled back slightly WoW, they were still insufficient to offset the rising pressure from aluminum scrap costs, leading to a continued increase in comprehensive production costs for enterprises, which in turn drove up offers. Demand side, past mid-October, orders for secondary aluminum plants remained stable. Although orders this month did not show significant growth compared to September, market performance was optimistic, and overall demand remained resilient. Coupled with low finished product inventories at manufacturers and ongoing pressure for order fulfillment, this provided some support to market prices. Supply side, factors constraining the operating rate persisted, including insufficient raw material circulation, high-priced raw materials eroding profits and forcing production cuts, as well as continued production halts due to unclear policies in regions such as Jiangxi and Anhui. Inventory side, social inventory of secondary aluminum alloy ingots in mainstream consumption areas stood at 54,700 mt on October 23, down 100 mt WoW, marking a weak destocking trend for two consecutive weeks. Recently, warehouse inflows of alloy ingots by traders have been low, while feedback indicated improved shipments of aluminum alloy ingots, especially non-standard products, driving the destocking of social inventory. In the short term, supported by rigid cost pressures and a tight supply-demand balance, ADC12 aluminum alloy ingot prices are expected to hold up well. Subsequent attention should focus on raw material supply, consumption performance, and inventory changes.